Materiality

Reporting on Sustainability is Evolving out of Tens of Pages of Stories and into More Decision-Useful and Industry-Specific Accounting Metrics

The SEC (Securities and Exchange Commission) has defined Materiality as information “to which there is a substantial likelihood that a reasonable investor would attach importance in determining whether to buy or sell the securities registered.” Under regulation S-K, the SEC gives publicly traded companies reporting requirements on material factors to form 10-K.

The same ESG topic may be material for many sectors yet manifest differently across industries – and so the need for industry-specific metrics. For example, flash floods in Southeast Asia may affect the supply chain for a wide range of industries (i.e. chip manufacturers, textiles, and agricultural products). Meanwhile, other industries would need accounting metrics to manage direct costs (i.e. hotels, hospitals, insurers). Strong ESG policies – with its corresponding metrics – may help mitigate such risks and more quickly respond to challenges.

Considering material ESG issues is not for risk and cost reduction purposes alone. Organizations who are able to prioritize and lead in their industry-specific sustainability topics may enhance their brand reputation across the value chain – potentially resulting in lower cost of capital from lenders and lower rates from insurers as well as increased customer loyalty and revenue.

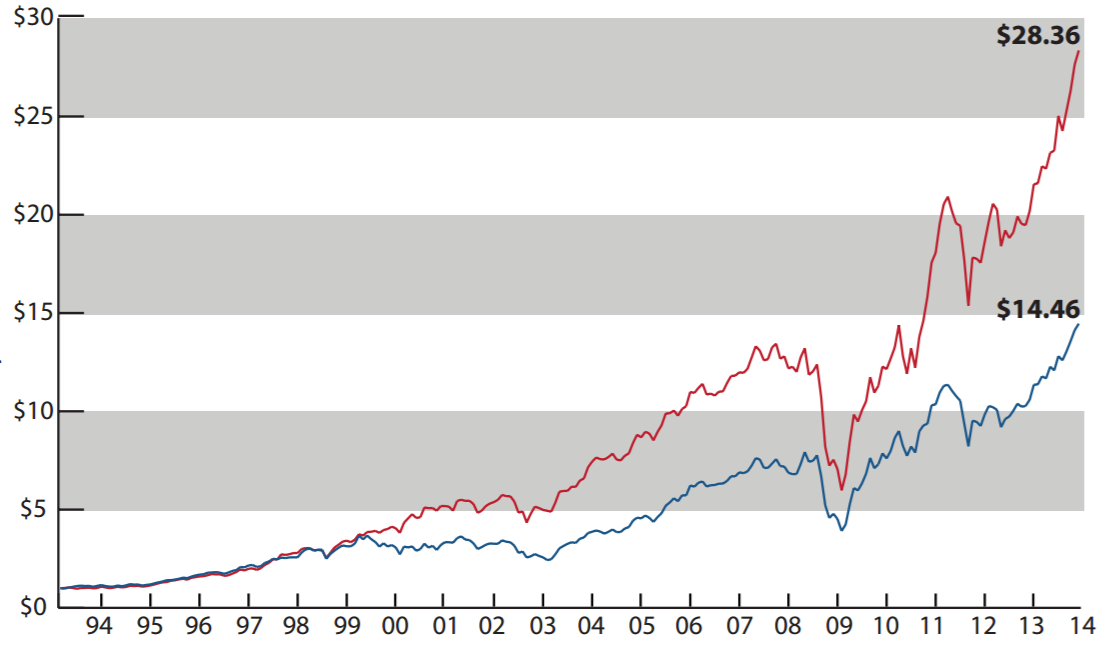

Value of 1USD Invested in 1993

(click on the image to access the report)

The figure shows the evolution of $1 invested in a portfolio of firms with high performance on material sustainability issues versus competitor firms with low performance on material sustainability issues. Materiality of sustainability issues is industry-specific and it is defined by the Sustainability Accounting Standards Board.

Source: Eccles, Robert G., Ioannis Ioannou, and George Serafeim. "The Impact of Corporate Sustainability on Organizational Processes and Performance." Management Science 60, no. 11 (November 2014): 2835–2857

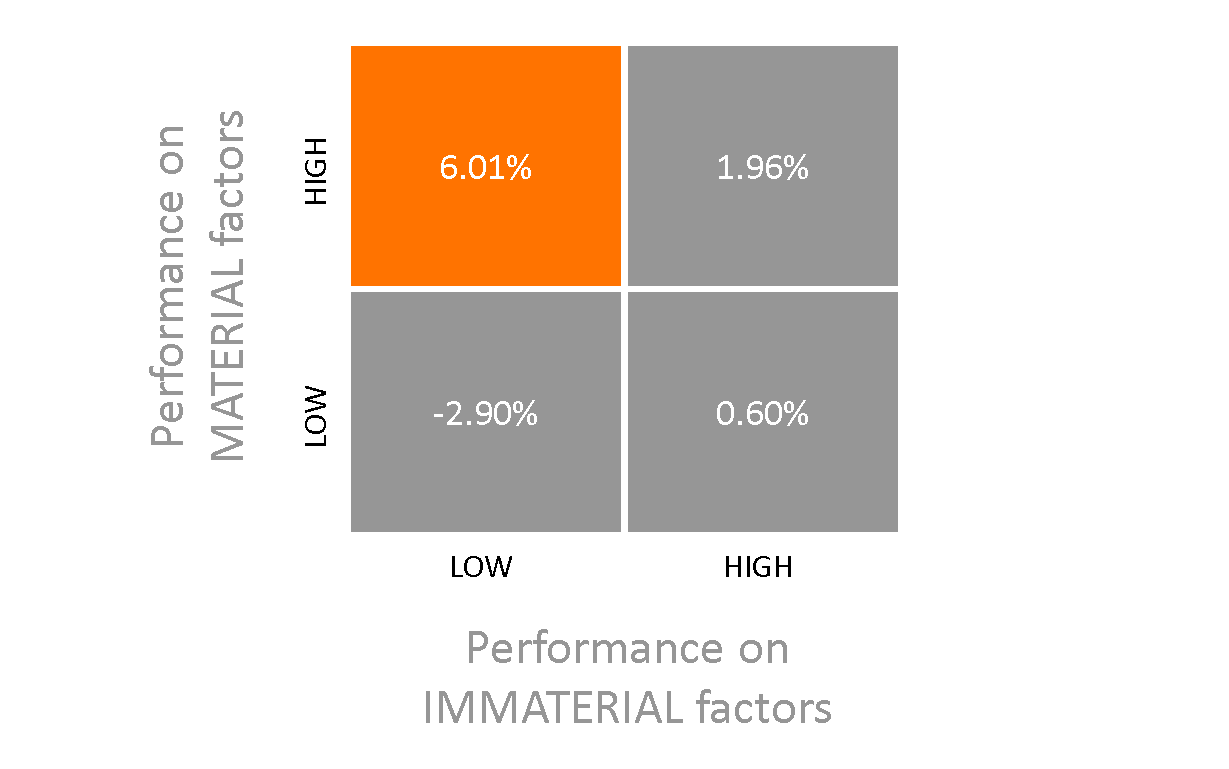

Stock Returns (in annualized alpha) by Type of Sustainability Performance

(click on the image to access the report from SASB)

Source: Khan, Mozaffar, George Serafeim, and Aaron Yoon. "Corporate Sustainability: First Evidence on Materiality." Harvard Business School Working Paper. March 2015. As published by SASB.

Are your ESG policies Material?

Carlos can help you understand the significance and implications of looking at Sustainability initiatives through the lens of Materiality!